The insurance industry is a major component of the economy by virtue of the number of premiums it collects, the scale of its investment and, more fundamentally, the essential social and economic role it plays by covering personal and business risks.

The global insurance market faces a truly unique moment in its history. The fundamental disruption caused by the COVID-19 pandemic equates to an opportunity for the industry to remake itself in line with new societal realities and market needs.

Maturing markets, tight capital, increasing risk and technologically sophisticated customers are just some of the pressures the insurance sector faces today. The global insurance industry is at a watershed moment. Insurance leaders have witnessed the growing impact of fintechs – financial technology startups – who invest in insurance technology (insurtechs).

Overview of the Global Insurance Sector

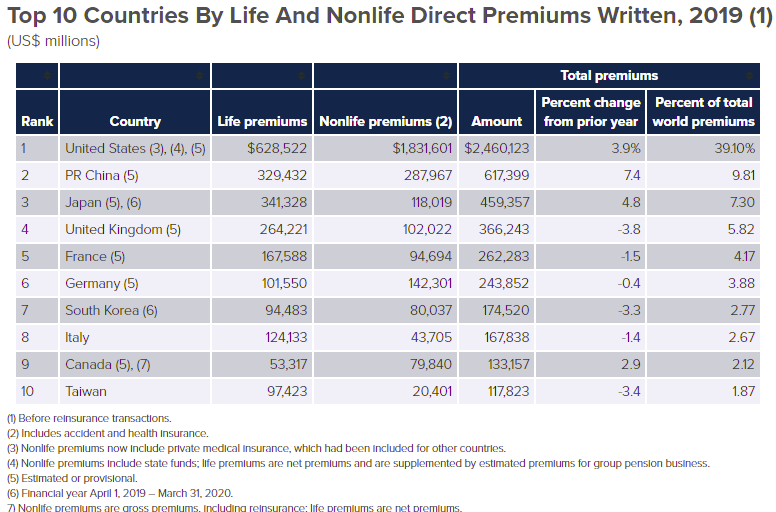

The insurance industry is divided into life and nonlife (or general insurance); the value of the market is shown in terms of gross premium incomes. The life insurance sector consists of mortality protection and annuity. The nonlife insurance sector consists of accident, health, property and casualty insurance segments.

World insurance premiums rose 3% in 2019, adjusted for inflation, to $5.1 trillion.

Nonlife premiums grew 3.5% in 2019, adjusted for inflation, slightly above the growth rate from 2009 to 2018.

Life insurance premiums grew 2.2% in 2019, faster than the 1.5% rise in 2009 to 2018, adjusted for inflation.

How the COVID-19 pandemic changed customer needs:

The year 2020 will forever be associated with the pandemic. The insurance industry experienced broad and deep impacts — financially, operationally, strategically — as COVID-19 brought the future forward, accelerating many trends that had been long underway. The effects will be felt for years to come.

However, surprising developments present opportunities. The dramatic spike in the interest of younger generations in life, health and other protection products is an encouraging demand signal. The demonstrated ability of insurers to move quickly and boldly in upgrading digital capabilities bodes well for the future. Insurers must work to ensure that customers better understand their products if they are to capitalize on the new demand.

Businesses must concurrently manage three crucial phases of the COVID-19 crisis—respond, recover, and thrive. When the pandemic emerged, insurers responded by taking immediate steps to ensure business continuity and help customers and their communities cope. As they head into 2021, insurers should consider a mix of offensive and defensive actions to accelerate longer-term recovery efforts and pivot to the thrive phase when growth is reemphasized, despite challenging economic conditions.

Tech and insurance industry – INSURTECH

After a long period of slow change, the insurance industry is finally following suit. Leading insurance businesses are starting to better connect risk with customers by partnering with or being inspired by dynamic new startups – insurtechs – across the insurance sector.

Insurtechs are typically technology-oriented startups that use innovative technical solutions to power new insurance business models. They take advantage of inefficiencies, substituting parts or all of the insurance value chain, and often get between traditional industry players and customers and their risks.

Insurtechs are also actively engaged in innovating traditional insurance business models.

The global insurtech market size was valued at $ 2.7 billion in 2020.

It is expected to expand at a compound annual growth rate (CAGR) of 48.8% from 2021 to 2028.

That means a market worth $ 3.6 billion by 2021 and more than 61 billion by 2028.

Insurtechs and the venture capitalists who fund them are looking to accelerate a shift of the industry away from traditional insurance products toward personal risk management, micro products and insurance-as-a-service. Individuals can employ these to manage their own risk rather than pay whole premiums for insurance companies to care for them.

The increasing need for digitization of insurance services is expected to propel market growth. Simplification of the claims processes is anticipated to drive the change. Insurance companies are focusing on improving communication with their clients and capabilities to implement automation processes. They are also focusing on using these solutions as they use technology innovations mainly designed to enhance the efficiency of the existing insurance industry model. These solutions are helping businesses discover avenues that large insurance companies have less incentive to achieve, such as offering social insurance and ultra-customized policies. These solutions use new streams of information from the internet-enabled devices to price premiums according to observed behaviour.

Insurtech is the usage of innovations particularly designed to make the existing insurance model more efficient. By using technologies such as AI and data analytics, insurtech solutions allow products to be priced more competitively. Insurance companies are widely adopting these solutions to drive cheaper, better, and faster operational results. Hence, the insurance industry is witnessing increased investment in technology.

The outbreak of COVID-19 is anticipated to have a positive impact on the market. Numerous insurance companies are reconsidering their long-term strategies and short-term needs. The COVID-19 and its consequences are accelerating the implementation of online platforms and new mobile applications to meet consumer needs.

Overview of the Automotive Insurance Sector

As per the report published by Allied Market Research, the global auto insurance market generated $740 billion in 2019 and is anticipated to hit $1.1 trillion by 2027, registering a CAGR of 8.5% from 2020 to 2027.

Ø The rise in the number of accidents, implementation of stringent government regulation for the adoption of auto insurance, and surge in automobile sales across the globe drive the growth of the global auto insurance market.

Ø Auto insurance is a contract between the insurance company and vehicle owners that protects them against financial loss in the event of vehicle theft or accident. The insurance company agrees to pay the covered amount of the losses in exchange for paying a premium.

Increasing awareness among end-users, introducing innovative technologies and products, and the availability of third-party insurance providers are to deploy substantial traction for the automotive insurance industry over the forecast period. Automotive insurance companies work with software providers to offer big data-based solutions to satisfy the end user’s concerns and untapped market demand during a car-related transaction.

Furthermore, digital technologies and mobile internet are transforming the vehicle industry and the vehicle/automotive insurance industry. The automotive industry is undoubtedly undergoing significant changes that will help increase asset utilization, change vehicle ownership models, and improve vehicle safety, which will eventually impact the global automotive insurance market. Additionally, autonomous technology has made cars increasingly safer, which is expected to reduce vehicle accidents significantly during the forecast period. Moreover, a rise in on-demand transportation and the shifting of liability to manufacturers are some of the factors that are expected to hinder the growth of global automotive insurance during the forecast period.

Key Drivers of Automotive Insurance Market

Automotive safety has become a significant concern amidst a consistent rise in the number of accidents across the globe due to the high number of on-road vehicles, unsafe driving patterns, underdeveloped infrastructure, and numerous other such factors. In February 2020, according to the World Health Organization, 1.35 million people died every year across the globe, costing a majority of countries around 3% of their total GDP. This economic burden, caused by the growing number of accidents, severely impacts low-income individuals and nations. Consequently, vehicle owners prefer insurance policies to mitigate this financial burden of road accidents, covering health-related and vehicle repair costs post-accident. Thus, a rise in awareness about road traffic accidents and their economic costs drives the global automotive insurance market.

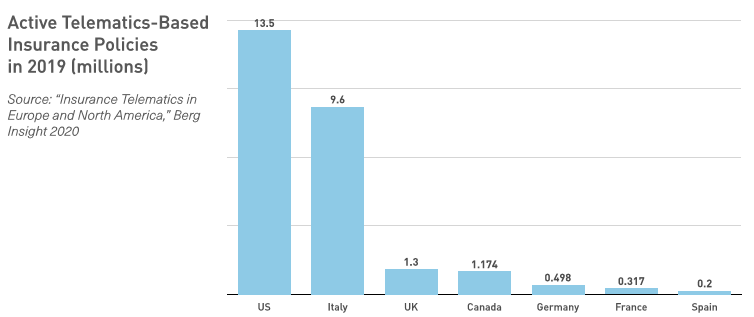

The emergence of the latest technologies, such as Internet of Things (IoT) and artificial intelligence, has transformed conventional auto insurance policies into usage-based policies. Sensors powered by these advanced technologies are fitted on vehicles to monitor the driving behaviour and pattern of the driver. This data is sent to the insurance company, and based on this data, the premium of insurance is modified. These new telematics-based insurance policies are gaining high popularity, hence fuelling the automotive insurance market across the globe.

Insurtech in the automotive sector:

Aside from health and life coverage, there can be few areas more appropriate for insurtech to assert a benevolent – and mutually beneficial – influence on the behaviour of policyholders than in the area of auto coverage.

Telematics offers much more than access to coverage for high-risk groups above and below a certain age. It can reward all policyholders with lower premiums if they are prepared to reduce risk by adjusting their behaviour behind the wheel.

As these systems are developed, telematics will likely have an increasing role to play within underwriting and pricing. The nature of insurance is changing globally, as individuals tend to lease or rent cars and are offered a whole of life service. This is expected to include auto coverage automatically as manufacturers operate like a distribution platform.

Connected devices are becoming a prominent part of our daily lives, and many businesses are trying to figure out how they can exploit this trend to create a deeper relationship with their customers. Motor insurers are not immune to the changes that are happening, primarily as they operate in an increasingly competitive market.

Deloitte has recently conducted a detailed analysis and report, which estimates that in Western Europe, the market share for digitally-enabled motor insurance by 2020 could exceed 15 billion Euros. From this study, they concluded that the “big-switch” is coming; digitally-enabled motor insurance is a crucial differentiator in a frequently commoditized market.

Historically, the target of insurers for their telematics product has been young drivers paying high premiums. However, these customers are not the only group who may be interested in digitally-enabled motor insurance.

The influence of data privacy on purchasing decisions by customers is quite significant but varies across Europe. Interestingly, customers appear to be much more comfortable sharing driving data than social media data. This suggests that at present, it may be difficult for insurance companies to collect and use social media data, despite its potential for creating new contact points with existing customers. Unsurprisingly, price is the most significant driver of customer’s purchase decisions.

Through the launch of value-added services linked to digitally-enabled motor insurance products, insurers finally have the opportunity to differentiate their products and engage their customers in new ways, thereby helping to change their perceptions of insurance products and providers.

There are clear signs that customers across Europe would value a telematics offering!

The “Connect Insurance” Channel opportunity

The COVID crisis has started changing the automotive insurance industry:

81% of drivers in the UK have changed how much they drive because of COVID-19. Across Europe, the pandemic has also modified the reasons why people move, their driving patterns, and the nature of the pool of drivers on the road. The riskier drivers are now disproportionally driving more; a quarter of them are young drivers.

As a result, previous models are not representative of commuters’ risk during the succession of lockdowns. Without individual driver data, insurers’ traditional risk proxies are no longer predictive and may not return to the utility.

The COVID pandemic is pushing people towards transacting via online channels, which is now the prime transaction method for up to 63% of the drivers.

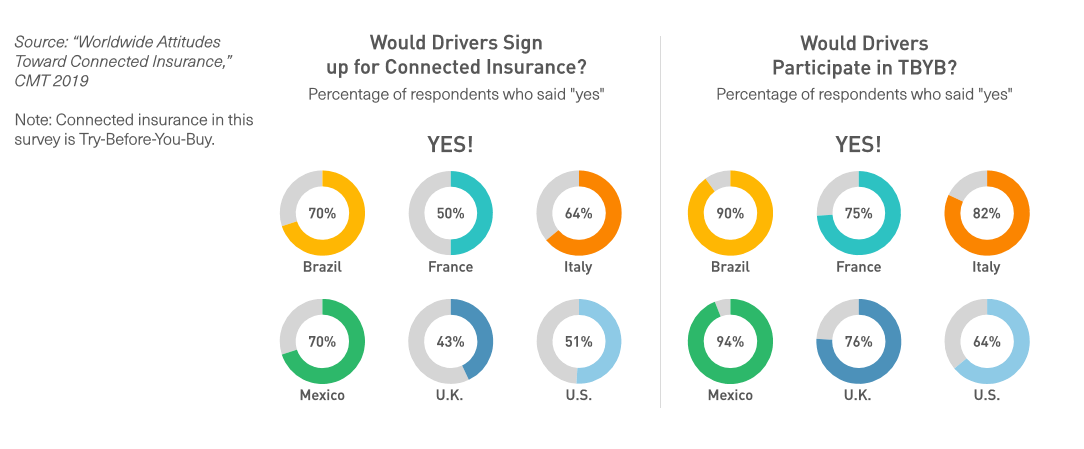

The appetite for connected insurance models has increased sharply since the pandemic started in Europe, with 65% of the population now likely to make the switch. In January 2020, “only” 49% of European drivers suggested it be possible to try usage-based insurance.

In terms of the value proposition and pricing models, the survey demonstrates a considerable shift away from “old school” discount-based telematics (-58%) to Pay-As-You-Drive (+145%) models.

The appetite for Value Added Services has also progressed, with safety-related options such as rewards for safe driving and emergency roadside assistance at the top of drivers’ wish lists. Claims assistance using automatically generated reports was a close second.

Consumers’ interest in telematics is at an all-time high – and growing. The COVID crisis brought home the benefits of telematics to many drivers. Since then, a flurry of positive articles has reinforced that telematics is the best way to save money on insurance.

The market and consumers are becoming more and more mature and ready to switch!

The original idea behind using telematics data in the insurance sector was to monitor a vehicle’s usage to price insurance based on the policyholder’s driving behaviour. Today, it allows insurance companies to reward those who opt into safe driving or distance-based programmes based on risky behaviours, scoring, and GPS monitoring.

As technology evolves, it allows for new, more robust business models. This has been particularly noticeable since smartphone-centric insurance has introduced a brand new direct and constant communication channel between the insurer and the insured.

Together with frequency and richness of interaction, connected insurance brings another benefit. By selecting the risks, influencing driving behaviour, and using the crash data efficiently during the claims handlings process, carriers are able to accelerate the claims management and benefit from increased efficiencies.

Connected insurance provides the drivers with the flexibility they now need since they drive less or differently. At the same time, it provides insurers with the information required to price risk appropriately.